Obama's legacy isn't just allowing the USA to be flooded with traitors but his destroying the American economy as well and not to mention his damage to the American military etc...

Men Without Work: Millions Missing From The Workforce

Why are so many men in their prime working years unemployed? The Obama administration would have us believe that unemployment is low in this country, but that is not true at all. In fact, one author quoted by NPR says that "it's kind of worse than it was in the depression in 1940.

Most Americans don't realize this, but more men from ages 25 to 54 are "inactive" right now than was the case during the last recession. We have millions upon millions of strong young men just sitting around doing nothing.

They aren't employed and they aren't considered to be looking for employment either, and so they don't show up in the official unemployment numbers. But they don't have jobs, and nothing the Obama administration does can eliminate that fact.

According to NPR, "nearly 100 percent of men between the ages of 25 and 54 worked" in the 1960s.

In those days, just about any dependable, hard working American man could get hired almost immediately. The economy was growing and the demand for labor was seemingly insatiable.

But today, one out of every six men in their prime working years does not have a job...

In a recent report, President Obama's Council of Economic Advisers said 83 percent of men in the prime working ages of 25-54 who were not in the labor force had not worked in the previous year. So, essentially, 10 million men are missing from the workforce.

"One in six prime-age guys has no job; it's kind of worse than it was in the depression in 1940," says Nicholas Eberstadt, an economic and demographic researcher at American Enterprise Institute who wrote the book Men Without Work: America's Invisible Crisis. He says these men aren't even counted among the jobless, because they aren't seeking work.

So why is this happening?

If you look at the inactivity rate for men in the 25 to 54 age bracket, it was sitting at just 8.1 percent in January 2000.

In January 2008, right at the beginning of the last recession, it was sitting at 9.2 percent, and by the end of the recession it had risen to 10.3 percent.

Today, it is sitting at 11.5 percent.

Remember, these are men that don't even count toward the official unemployment rate. They are not working, but they are not considered to be "looking for work" either.

So what are these men doing?

You may be tempted to think that many of them have decided to stay home and raise the kids as their wives go off to work. But according to NPR, that is not what is happening...

What the missing men aren't doing in large numbers is staying home to take care of family. Forty percent of nonworking women are primary caregivers; that's true of only 5 percent of men out of the workforce.

We do have the largest prison population in the entire world by far, and without a doubt that does play a role in these numbers. However, a far bigger factor is the millions of men that have become content being dependents of the federal government.

More than 100 million Americans receive money from the government each month, and a lot of people (both men and women) have found that it is just easier to sit back and collect government checks than it is to go out and try to work hard for a living.

But of course the number one factor is the lack of jobs available. I personally know people that have been looking for work in their fields for years and have not been able to get hired. We have a major employment crisis in this nation, and it is only going to get worse in the years ahead as we continue to lose jobs to technology and millions more good jobs get shipped overseas.

And a lot of the "jobs" that have been created during the Obama administration have been very low quality jobs. Since December 2014, we have gained about half a million jobs for waiters and bartenders, but meanwhile we have actually lost good paying manufacturing jobs. If we continue down this road, the middle class will continue to shrink.

In addition to everything that I have just shared, here are some other facts that are pertinent to this discussion...

-Right at this moment, there are approximately 102 million working age Americans that do not have a job.

-Nearly one out of every five young adults are currently living with their parents.

-The Wall Street Journal recently declared that this is the weakest "economic recovery" since 1949.

-Barack Obama is on track to be the only president in U.S. history to never have a single year when the U.S. economy grew by at least 3 percent.

The economy is far weaker than you are being told, the employment crisis is far worse than you are being told, and as I mentioned yesterday, the stage is clearly set for a new financial crisis of epic proportions.

And if we are going to see markets crash, this time of the year is a good time for it. In fact, CNBC says that history tells us that this is the "worst period of the year for stocks"...

The worst period of the year for stocks has just begun -- at least based on market history.

Over the entire 120-year history of the Dow Jones industrial average, Sept. 6 to Oct. 29 tends to be the worst period for the market. And more specifically, the last few weeks of September have been an especially bad time.

Someday when people look back at this time in history, they will not be surprised by how horrific the coming collapse will be. The truth is that anyone with a lick of common sense can see that the greatest debt bubble in the history of the world is going to end badly.

No, what is going to amaze them is that the system was able to hold together as long as it did. It truly is incredible that the debt-based, fiat currency Ponzi scheme that the central banks of the world have been desperately trying to prop up has been able to keep chugging along all the way to the middle of 2016.

How much longer can they keep the magic going?

I don't know, but history tells us that time is not on their side...

Read more at http://www.prophecynewswatch.com/articl ... YpAILbX.99

The Coming Financial Meltdown

Forum rules

Civil discussion appreciated. No Spam...

Civil discussion appreciated. No Spam...

Re: The Coming Financial Meltdown

Barack Hussein Obama has successfully damaged the american economy. This is probably one of his proudest accomplishments. Americans actually voted him in for a second term. At least he will hopefully be stepping down soon. The sooner the better for the non islamic world.

Time To Face The True State Of The Middle Class In America

By Michael Snyder/Economic Collapse Blog September 23, 2016

Do you remember the old Saturday Night Live sketches in which comedian Chris Farley portrayed a motivational speaker that lived in a van down by the river? Unfortunately, this is becoming a reality for way too many Americans. As the middle class has shrunk and the cost of living has increased, a lot of people have decided to quite literally "live on the road".

Whether it is a car, a truck, a van, a bus or an RV, an increasing number of Americans are using their vehicles as their homes. Just recently, someone that I know took a trip down the west coast of the United States and stayed at a number of campgrounds along the way.

What she discovered was that a lot of people were actually living at these campgrounds. Of course there are some that actually prefer that lifestyle, but many others are doing it out of necessity.

Earlier this week, Circa.com posted a story about "the van life". One of the individuals that they featured was a recent graduate of the University of Southern California named Stephen Hutchins. Without much of an income at the moment, he decided that the best way to cut expenses was to live in his van...

"The main expenses are insurance for the van, which is like $60 a month," said Hutchins. "Then, I have a storage unit for like $60."

That puts his monthly rent at $120. The van cost him just $125 at an auction.

Living in a van is certainly not the most comfortable way to go, and many of you are probably wondering how he performs basic tasks such as cooking and bathing. Well, it turns out that he makes extensive use of public facilities...

He showers at the gym, cooks on a portable stove on a sidewalk (he stores his butane at his friends' place nearby) and uses wifi at nearby coffeeshops.

For a while such a lifestyle may seem like "an adventure", but after a while it will start to get really old. And not a lot of women are going to be excited about dating a man that lives in a van, and you certainly wouldn't want to raise a family in a vehicle.

Sadly, just like during the last economic crisis many Americans are getting to the point where staying in their homes may not be an option. Just check out the following excerpt from a recent New York Post article entitled "The terrifying signs of a looming housing crisis"...

The number of New Yorkers applying for emergency grants to stay in their homes is skyrocketing -- as the number of people staying in homeless shelters reached an all-time high last weekend, records show.

There were 82,306 applications for one-time emergency grants to prevent evictions in fiscal 2016, up 26 percent from 65,138 requests the previous year, according to the Mayor's Management Report.

First of all, it is very alarming to hear that the number of New Yorkers staying in homeless shelters "reached an all-time high" last weekend. I thought that we were supposed to be in an "economic recovery", but apparently things in New York are rapidly getting worse.

Secondly, the fact that applications for emergency grants are up 26 percent compared to last year is another indication of how rough things are right now for average families in New York. We all remember what happened when millions of families lost their homes to foreclosure across the nation during the last financial crisis, and nobody should want to see a repeat of that any time soon.

During this election season, Barack Obama and Hillary Clinton would like all of us to believe that the economy is doing just fine, but that is not true at all.

Even using the doctored numbers that the government gives us, Barack Obama is solidly on track to be the only president in all of U.S. history to never have a single year of 3 percent GDP growth, and he has had two terms to try to do that.

Gallup CEO Jim Clifton is also quite skeptical of this "economic recovery", and he recently authored an article on this subject that is receiving a tremendous amount of attention. The following is how that article begins...

I've been reading a lot about a "recovering" economy. It was even trumpeted on Page 1 of The New York Times and Financial Times last week.

I don't think it's true.

The percentage of Americans who say they are in the middle or upper-middle class has fallen 10 percentage points, from a 61% average between 2000 and 2008 to 51% today.

Other surveys have found that it is even worse than that.

For example, a Pew Research Center study from the end of last year discovered that the middle class in America has now actually become a minority in this country.

Here are some other numbers that Clifton included in his article...

According to the U.S. Bureau of Labor Statistics, the percentage of the total U.S. adult population that has a full-time job has been hovering around 48% since 2010 -- this is the lowest full-time employment level since 1983.

The number of publicly listed companies trading on U.S. exchanges has been cut almost in half in the past 20 years -- from about 7,300 to 3,700. Because firms can't grow organically -- that is, build more business from new and existing customers -- they give up and pay high prices to acquire their competitors, thus drastically shrinking the number of U.S. public companies. This seriously contributes to the massive loss of U.S. middle-class jobs.

New business startups are at historical lows. Americans have stopped starting businesses. And the businesses that do start are growing at historically slow rates.

Once upon a time, America was the land of opportunity.

We were the place where anything was possible and where entrepreneurship was greatly encouraged.

But today we strangle small businesses to death with rules, regulations, red tape and taxes.

If we want a stronger middle class, we need to create a much better environment for the creation of small businesses. Small business ownership often lifts individuals into the middle class, and small businesses have traditionally been the primary engine for the growth of good jobs in this country.

If the middle class continues to shrink, poverty will continue to rise. Previously I have written about how the number of homeless children in the United States has shot up by 60 percent since the last economic crisis, and Poverty USA claims that a staggering 1.6 million children slept either in a homeless shelter or in some other form of emergency housing during 2015.

If you will be sleeping in a warm bed in a comfortable home tonight, you should be thankful. An increasing number of Americans are sleeping in tent cities, in their vehicles or on the streets. These hurting people deserve our love, our compassion and our prayers.

Read more at http://www.prophecynewswatch.com/articl ... KQDSBM0.99

Time To Face The True State Of The Middle Class In America

By Michael Snyder/Economic Collapse Blog September 23, 2016

Do you remember the old Saturday Night Live sketches in which comedian Chris Farley portrayed a motivational speaker that lived in a van down by the river? Unfortunately, this is becoming a reality for way too many Americans. As the middle class has shrunk and the cost of living has increased, a lot of people have decided to quite literally "live on the road".

Whether it is a car, a truck, a van, a bus or an RV, an increasing number of Americans are using their vehicles as their homes. Just recently, someone that I know took a trip down the west coast of the United States and stayed at a number of campgrounds along the way.

What she discovered was that a lot of people were actually living at these campgrounds. Of course there are some that actually prefer that lifestyle, but many others are doing it out of necessity.

Earlier this week, Circa.com posted a story about "the van life". One of the individuals that they featured was a recent graduate of the University of Southern California named Stephen Hutchins. Without much of an income at the moment, he decided that the best way to cut expenses was to live in his van...

"The main expenses are insurance for the van, which is like $60 a month," said Hutchins. "Then, I have a storage unit for like $60."

That puts his monthly rent at $120. The van cost him just $125 at an auction.

Living in a van is certainly not the most comfortable way to go, and many of you are probably wondering how he performs basic tasks such as cooking and bathing. Well, it turns out that he makes extensive use of public facilities...

He showers at the gym, cooks on a portable stove on a sidewalk (he stores his butane at his friends' place nearby) and uses wifi at nearby coffeeshops.

For a while such a lifestyle may seem like "an adventure", but after a while it will start to get really old. And not a lot of women are going to be excited about dating a man that lives in a van, and you certainly wouldn't want to raise a family in a vehicle.

Sadly, just like during the last economic crisis many Americans are getting to the point where staying in their homes may not be an option. Just check out the following excerpt from a recent New York Post article entitled "The terrifying signs of a looming housing crisis"...

The number of New Yorkers applying for emergency grants to stay in their homes is skyrocketing -- as the number of people staying in homeless shelters reached an all-time high last weekend, records show.

There were 82,306 applications for one-time emergency grants to prevent evictions in fiscal 2016, up 26 percent from 65,138 requests the previous year, according to the Mayor's Management Report.

First of all, it is very alarming to hear that the number of New Yorkers staying in homeless shelters "reached an all-time high" last weekend. I thought that we were supposed to be in an "economic recovery", but apparently things in New York are rapidly getting worse.

Secondly, the fact that applications for emergency grants are up 26 percent compared to last year is another indication of how rough things are right now for average families in New York. We all remember what happened when millions of families lost their homes to foreclosure across the nation during the last financial crisis, and nobody should want to see a repeat of that any time soon.

During this election season, Barack Obama and Hillary Clinton would like all of us to believe that the economy is doing just fine, but that is not true at all.

Even using the doctored numbers that the government gives us, Barack Obama is solidly on track to be the only president in all of U.S. history to never have a single year of 3 percent GDP growth, and he has had two terms to try to do that.

Gallup CEO Jim Clifton is also quite skeptical of this "economic recovery", and he recently authored an article on this subject that is receiving a tremendous amount of attention. The following is how that article begins...

I've been reading a lot about a "recovering" economy. It was even trumpeted on Page 1 of The New York Times and Financial Times last week.

I don't think it's true.

The percentage of Americans who say they are in the middle or upper-middle class has fallen 10 percentage points, from a 61% average between 2000 and 2008 to 51% today.

Other surveys have found that it is even worse than that.

For example, a Pew Research Center study from the end of last year discovered that the middle class in America has now actually become a minority in this country.

Here are some other numbers that Clifton included in his article...

According to the U.S. Bureau of Labor Statistics, the percentage of the total U.S. adult population that has a full-time job has been hovering around 48% since 2010 -- this is the lowest full-time employment level since 1983.

The number of publicly listed companies trading on U.S. exchanges has been cut almost in half in the past 20 years -- from about 7,300 to 3,700. Because firms can't grow organically -- that is, build more business from new and existing customers -- they give up and pay high prices to acquire their competitors, thus drastically shrinking the number of U.S. public companies. This seriously contributes to the massive loss of U.S. middle-class jobs.

New business startups are at historical lows. Americans have stopped starting businesses. And the businesses that do start are growing at historically slow rates.

Once upon a time, America was the land of opportunity.

We were the place where anything was possible and where entrepreneurship was greatly encouraged.

But today we strangle small businesses to death with rules, regulations, red tape and taxes.

If we want a stronger middle class, we need to create a much better environment for the creation of small businesses. Small business ownership often lifts individuals into the middle class, and small businesses have traditionally been the primary engine for the growth of good jobs in this country.

If the middle class continues to shrink, poverty will continue to rise. Previously I have written about how the number of homeless children in the United States has shot up by 60 percent since the last economic crisis, and Poverty USA claims that a staggering 1.6 million children slept either in a homeless shelter or in some other form of emergency housing during 2015.

If you will be sleeping in a warm bed in a comfortable home tonight, you should be thankful. An increasing number of Americans are sleeping in tent cities, in their vehicles or on the streets. These hurting people deserve our love, our compassion and our prayers.

Read more at http://www.prophecynewswatch.com/articl ... KQDSBM0.99

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

Spreading the wealth, let everyone be paid the same, and lets have social justice over democracy.

That's until the money is gone, and you have government in full control to do with you as they wish.

That's until the money is gone, and you have government in full control to do with you as they wish.

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

Re: The Coming Financial Meltdown

Obama has plenty of cash. I think he likes Americans suffering.

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

He, and others like the Hollywood crowd fancy themselves as the ruling cast over the unwashed masses.

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

Re: The Coming Financial Meltdown

Is the USA still a free nation ? Bush and Obama have really changed America from the country I hitch hiked around over thirty years ago. Now they are trying to make it impossible for Americans to live free overseas! Will the next president make it a triple whammy ?

The Government Is Turning the Entire United States Into A Debt Prison

Since the United States was founded, citizenship has represented a safe haven from oppressive regimes around the world. By preserving the principles of small government and free markets, those who were willing to work hard found success, and America became a magnet for innovation.

But as the U.S. continues to erode personal and economic freedom, more people than ever before are handing over their U.S. passports to seek better opportunities abroad.

The staggering amount of debt held by the American empire ensures the public will be working it off for generations to come. The government has already begun its campaign to make it more difficult to leave the country, and it has also begun to crack down on the finances of the eight million Americans living abroad.

Regardless of whether you're a millionaire with multiple foreign bank accounts or a recent college graduate with a boatload of debt, the status of being a United States citizen brings with it a burden that will only grow heavier over time.

Since 2008, the number of individuals giving up their citizenship has increased by almost 560%, setting new records each of the past three years. Some of these expats are motivated by the extra tax load paid when working abroad while others are trying to avoid student loan debt. Others have just had enough of the encroaching police state.

Every taxpayer left in the country now owes more than $149,000 of the national debt, so it's no surprise the tide is beginning to turn. By hook or by crook, in the coming years, citizens will be fleeced of that money through higher taxes, savings that are inflated away, and an overall drop in their standard of living.

Many can see the writing on the wall and have become determined to protect themselves from the years of economic repression coming down the pipe.

Draconian steps have already been taken to slow the rate of expatriation. For one, the IRS has broadened its reach into foreign bank accounts through the Foreign Account Tax Compliance Act.

Through agreements with over 100 nations, the law is able to require all financial institutions abroad to report the account details of any American customers they have. With access to this new information, the IRS can revoke the passports of potential tax evaders and hinder their ability to travel using yet another additional power the agency was granted last year.

The Internal Revenue Service is one of the most powerful agencies of the federal government and has a track record of persecuting groups for political reasons. The fact that they have now set their sights are expats shouldn't surprise anyone.

The Tea Party movement, whatever your views on it, experienced this first-hand during the 2012 elections. Jenny Beth Martin, national coordinator of Tea Party Patriots spoke on the targeting scandal:

"The IRS has demonstrated the most disturbing, illegal and outrageous abuse of government power. This deliberate targeting and harassment of tea party groups reaches a new low in illegal government activity and overreach."

While penalties are being levied against those with enough money to work around the world, the most impactful measures are aimed at those just making ends meet. The initial paperwork for renouncing citizenship used to cost just $450, but it has skyrocketed to $2,350, making it the most expensive fee of any country in the world.

It may not seem like much in the grand scheme of things, but this additional expense directly targets the young and working class, creating a huge barrier to even starting the process. As an added bonus, the price increase has raised over $12 million for government coffers in just over a year.

The $19.5 trillion in debt that has been amassed through decades of interventionist policies and clandestine operations can only be maintained by taxing the government's human livestock. After all, the federal government counts student loans as almost 30% of their net worth.

If the young and productive workers of the future are allowed to leave, U.S. power and wealth will go with them.

The Millennial generation has been completely duped by the federal loan programs, pumped out to any 18-year-old with a pulse. The $1.3 trillion in outstanding student loans is akin to indentured servitude for those entering the dismal job market.

And students themselves aren't the only ones on the chopping block -- 90% of these loans are co-signed by the parents, attaching the ball and chain further up the family tree.

For those tempted to jump ship and disappear into another country, their families will be held responsible in their stead. It's reminiscent of North Korea, where the families of defectors are punished.

Noah Brown, president of the Association of Community College Trustees wrote:

"If you default, your financial life is ruined. You have to deal in cash for the rest of your life. It used to be death and taxes were the only certainty. You can throw in student loans now."

Many are learning the hard way that these loans are unique and can't be wiped away by simply declaring bankruptcy. Instead of the collateral being a house or a car, it's future earnings that can be seized.

Those who find themselves with no way out have been offered a deal with the devil -- work in the public sector for 10 years and you will be granted your freedom. This has created a perverse incentive to work directly for the state, placing fresh cogs in the military, police, and bureaucratic machines.

The policies seen so far are soft measures compared to what may be tried in the future as the government grows and the economy weakens.

A new type of debt prison is being built in the U.S., and as the inmates realize their predicament, the rush for the exits could be chaotic -- so long as people can afford to pay the fee to leave.

Those who understand the fragile state of our economic and political system can see that when politicians start building walls, it may be more about keeping people in than out.

Despite the brainwashing often conducted in public schools, many are realizing the future for U.S. citizens may look very different than the past.

The freedom and opportunity that have been synonymous with U.S. citizenship are being transformed before our eyes. When America abandoned its core values and let loose the scourge of oppressive big government, the countdown to when citizens would pay the price began.

Originally published at theAntimedia.org - reposted with permission.

Read more at http://www.prophecynewswatch.com/articl ... OtET8sR.99

The Government Is Turning the Entire United States Into A Debt Prison

Since the United States was founded, citizenship has represented a safe haven from oppressive regimes around the world. By preserving the principles of small government and free markets, those who were willing to work hard found success, and America became a magnet for innovation.

But as the U.S. continues to erode personal and economic freedom, more people than ever before are handing over their U.S. passports to seek better opportunities abroad.

The staggering amount of debt held by the American empire ensures the public will be working it off for generations to come. The government has already begun its campaign to make it more difficult to leave the country, and it has also begun to crack down on the finances of the eight million Americans living abroad.

Regardless of whether you're a millionaire with multiple foreign bank accounts or a recent college graduate with a boatload of debt, the status of being a United States citizen brings with it a burden that will only grow heavier over time.

Since 2008, the number of individuals giving up their citizenship has increased by almost 560%, setting new records each of the past three years. Some of these expats are motivated by the extra tax load paid when working abroad while others are trying to avoid student loan debt. Others have just had enough of the encroaching police state.

Every taxpayer left in the country now owes more than $149,000 of the national debt, so it's no surprise the tide is beginning to turn. By hook or by crook, in the coming years, citizens will be fleeced of that money through higher taxes, savings that are inflated away, and an overall drop in their standard of living.

Many can see the writing on the wall and have become determined to protect themselves from the years of economic repression coming down the pipe.

Draconian steps have already been taken to slow the rate of expatriation. For one, the IRS has broadened its reach into foreign bank accounts through the Foreign Account Tax Compliance Act.

Through agreements with over 100 nations, the law is able to require all financial institutions abroad to report the account details of any American customers they have. With access to this new information, the IRS can revoke the passports of potential tax evaders and hinder their ability to travel using yet another additional power the agency was granted last year.

The Internal Revenue Service is one of the most powerful agencies of the federal government and has a track record of persecuting groups for political reasons. The fact that they have now set their sights are expats shouldn't surprise anyone.

The Tea Party movement, whatever your views on it, experienced this first-hand during the 2012 elections. Jenny Beth Martin, national coordinator of Tea Party Patriots spoke on the targeting scandal:

"The IRS has demonstrated the most disturbing, illegal and outrageous abuse of government power. This deliberate targeting and harassment of tea party groups reaches a new low in illegal government activity and overreach."

While penalties are being levied against those with enough money to work around the world, the most impactful measures are aimed at those just making ends meet. The initial paperwork for renouncing citizenship used to cost just $450, but it has skyrocketed to $2,350, making it the most expensive fee of any country in the world.

It may not seem like much in the grand scheme of things, but this additional expense directly targets the young and working class, creating a huge barrier to even starting the process. As an added bonus, the price increase has raised over $12 million for government coffers in just over a year.

The $19.5 trillion in debt that has been amassed through decades of interventionist policies and clandestine operations can only be maintained by taxing the government's human livestock. After all, the federal government counts student loans as almost 30% of their net worth.

If the young and productive workers of the future are allowed to leave, U.S. power and wealth will go with them.

The Millennial generation has been completely duped by the federal loan programs, pumped out to any 18-year-old with a pulse. The $1.3 trillion in outstanding student loans is akin to indentured servitude for those entering the dismal job market.

And students themselves aren't the only ones on the chopping block -- 90% of these loans are co-signed by the parents, attaching the ball and chain further up the family tree.

For those tempted to jump ship and disappear into another country, their families will be held responsible in their stead. It's reminiscent of North Korea, where the families of defectors are punished.

Noah Brown, president of the Association of Community College Trustees wrote:

"If you default, your financial life is ruined. You have to deal in cash for the rest of your life. It used to be death and taxes were the only certainty. You can throw in student loans now."

Many are learning the hard way that these loans are unique and can't be wiped away by simply declaring bankruptcy. Instead of the collateral being a house or a car, it's future earnings that can be seized.

Those who find themselves with no way out have been offered a deal with the devil -- work in the public sector for 10 years and you will be granted your freedom. This has created a perverse incentive to work directly for the state, placing fresh cogs in the military, police, and bureaucratic machines.

The policies seen so far are soft measures compared to what may be tried in the future as the government grows and the economy weakens.

A new type of debt prison is being built in the U.S., and as the inmates realize their predicament, the rush for the exits could be chaotic -- so long as people can afford to pay the fee to leave.

Those who understand the fragile state of our economic and political system can see that when politicians start building walls, it may be more about keeping people in than out.

Despite the brainwashing often conducted in public schools, many are realizing the future for U.S. citizens may look very different than the past.

The freedom and opportunity that have been synonymous with U.S. citizenship are being transformed before our eyes. When America abandoned its core values and let loose the scourge of oppressive big government, the countdown to when citizens would pay the price began.

Originally published at theAntimedia.org - reposted with permission.

Read more at http://www.prophecynewswatch.com/articl ... OtET8sR.99

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

It started earlier though, Johnson for sure, Nixon with China, and the gold standard, Clinton also selling us out in several ways.

Bush, and Obama though, they have transformed us into an Orwellian society with spy cameras, and hurt feelings being a crime.

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

Great job Obama, we knew you could do it.

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

Re: The Coming Financial Meltdown

Obama really nails the straight face while he does his rosy state of the union lies.

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

All he does is lie, and still the masses believe him like the demented sick sheep they are. Hillary is a habitual lying person, and don't hide it anymore that she don't care, but people will follow her into the toilet .

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

Re: The Coming Financial Meltdown

I wonder what if Merkels influx of refugees has anything to do with this. They must be a severe drain on the German economy.

Deutsche Bank Collapse: The Most Important Bank In Europe On The Brink

The largest and most important bank in the largest and most important economy in Europe is imploding right in front of our eyes. Deutsche Bank is the 11th biggest bank on the entire planet, and due to the enormous exposure to derivatives that it has, it has been called "the world's most dangerous bank".

Over the past year, I have repeatedly warned that Deutsche Bank is heading for disaster and is a likely candidate to be "the next Lehman Brothers".

On September 16th, the Wall Street Journal reported that the U.S. Department of Justice wanted 14 billion dollars from Deutsche Bank to settle a case related to the mis-handling of mortgage-backed securities during the last financial crisis.

As a result of that announcement, confidence in the bank has been greatly shaken, the stock price has fallen to record lows, and analysts are warning that Deutsche Bank may be facing a "liquidity event" unlike anything that we have seen since the collapse of Lehman Brothers back in 2008.

At one point on Friday, Deutsche Bank stock fell below the 10 euro mark for the first time ever before bouncing back a bit. A completely unverified rumor that was spreading on Twitter that claimed that Deutsche Bank would settle with the Department of Justice for only 5.4 billion dollars was the reason for the bounce.

But the size of the fine is not really the issue now. Shares of Deutsche Bank have fallen by more than half so far in 2016, and this latest episode seems to have been the final straw for the deeply troubled financial institution. Old sources of liquidity are being cut off, and nobody wants to be the idiot that offers Deutsche Bank a new source of liquidity at this point.

As a result, Deutsche Bank is potentially facing a "liquidity event" on a scale that we have not seen since the financial crisis of 2008. The following comes from Zero Hedge...

It is not solvency, or the lack of capital - a vague, synthetic, and usually quite arbitrary concept, determined by regulators - that kills a bank; it is - as Dick Fuld will tell anyone who bothers to listen - the loss of (access to) liquidity: cold, hard, fungible (something Jon Corzine knew all too well when he commingled and was caught) cash, that pushes a bank into its grave, usually quite rapidly: recall that it took Lehman just a few days for its stock to plunge from the high double digits to zero.

It is also liquidity, or rather concerns about it, that sent Deutsche Bank stock crashing to new all time lows earlier today: after all, the investing world already knew for nearly two weeks that its capitalization is insufficient.

As we reported earlier this week, it was a report by Citigroup, among many other, that found how badly undercapitalized the German lender is, noting that DB's "leverage ratio, at 3.4%, looks even worse relative to the 4.5% company target by 20183 and calculated that while he only models ¬2.9bn in litigation charges over 2H16-2017 - far less than the $14 billion settlement figure proposed by the DOJ - and includes a successful disposal of a 70% stake in Postbank at end-2017 for 0.4x book he still only reaches a CET 1 ratio of 11.6% by end-2018, meaning the bank would have a Tier 1 capital ¬3bn shortfall to the company target of 12.5%, and a leverage ratio of 3.9%, resulting in an ¬8bn shortfall to the target of 4.5%.

The more the stock price drops, the faster other financial institutions, investors and regular banking clients are going to want to pull their money out of Deutsche Bank. And every time there is news about people pulling money out of the bank, that is just going to drive the stock price even lower.

In other words, Deutsche Bank may be entering a death spiral that may be impossible to stop without a government bailout, and the German government has already stated that there will be no bailout for Deutsche Bank.

Banking customers have a total of approximately 566 billion euros deposited with the bank, and even if a small fraction of those clients start demanding their money back it is going to cause a major, major crunch.

Deutsche Bank CEO John Cryan attempted to calm nerves on Friday by releasing a memo to employees that blamed "speculators" for the decline in the stock price...

Instead of doing what many have correctly suggested he should be doing, namely focusing on ways to raise more capital for the undercapitalized Deutsche Bank in order to stem the slow (at first) liquidity leak, first thing this morning CEO John Cryan issued another morale-boosting note to employees of Deustche Bank who have been watching their stock price crash to another record low, dipping under ¬10 in early trading for the first time ever.

In the memo the embattled CEO worryingly did what Dick Fuld and other chief executives did when they felt the situation slipping out of control, namely blaming evil "rumor-spreading" shorts, saying "our bank has become subject to speculation. Ongoing rumours are causing significant swings in our stock price. ... Trust is the foundation of banking. Some forces in the markets are currently trying to damage this trust."

Just as important, Cryan confirms the Bloomberg report that "a few of our hedge fund clients have reduced some activities with us. That is causing unjustified concerns."

As we explained last night, the concerns are very much justified if they spread to the biggest risk-factor for the German bank: its depositors, which collectively hold over ¬550 billion in liquidity-providing instruments.

One of the reasons why Deutsche Bank is considered to be so systemically "dangerous" is because it has 42 trillion euros worth of exposure to derivatives. That is an amount of money that is 14 times larger than the GDP of the entire nation of Germany.

Some firms that were derivatives clients of the bank have already gotten spooked and have moved their business to other institutions. It was this report from Bloomberg that really helped drive down the stock price of Deutsche Bank earlier this week...

The funds, a small subset of the more than 800 clients in the bank's hedge fund business, have shifted part of their listed derivatives holdings to other firms this week, according to an internal bank document seen by Bloomberg News.

Among them are Izzy Englander's $34 billion Millennium Partners, Chris Rokos's $4 billion Rokos Capital Management, and the $14 billion Capula Investment Management, said a person with knowledge of the situation who declined to be identified talking about confidential client matters.

"The issue here is now one of confidence," said Chris Wheeler, a financial analyst with Atlantic Equities LLP in London.

So what comes next?

Monday is a banking holiday for Germany, so we may not see anything major happen until Tuesday.

An announcement of a major reduction in the Department of Justice fine may buy Deutsche Bank some time, but any reprieve would likely only be temporary.

What appears to be more likely is the scenario that Jeffrey Gundlach is suggesting...

But Jeffrey Gundlach, chief executive of DoubleLine Capital, said investors betting that Berlin would not rescue Deutsche could find themselves nursing big losses.

'The market is going to push down Deutsche Bank until there is some recognition of support. They will get assistance, if need be,' said Gundlach, who oversees more than $100 billion at Los Angeles-based DoubleLine.

It will be very interesting to see how desperate things become before the German government finally gives in to the pressure.

The complete and total collapse of Deutsche Bank would be an event many times more significant for the global financial system than the collapse of Lehman Brothers was.

Global leaders simply cannot afford for such a thing to happen, but without serious intervention it appears that is precisely where we are heading.

Personally, I don't know exactly what will happen next, but it will be fascinating to watch

Read more at http://www.prophecynewswatch.com/articl ... ue6xUhV.99

Deutsche Bank Collapse: The Most Important Bank In Europe On The Brink

The largest and most important bank in the largest and most important economy in Europe is imploding right in front of our eyes. Deutsche Bank is the 11th biggest bank on the entire planet, and due to the enormous exposure to derivatives that it has, it has been called "the world's most dangerous bank".

Over the past year, I have repeatedly warned that Deutsche Bank is heading for disaster and is a likely candidate to be "the next Lehman Brothers".

On September 16th, the Wall Street Journal reported that the U.S. Department of Justice wanted 14 billion dollars from Deutsche Bank to settle a case related to the mis-handling of mortgage-backed securities during the last financial crisis.

As a result of that announcement, confidence in the bank has been greatly shaken, the stock price has fallen to record lows, and analysts are warning that Deutsche Bank may be facing a "liquidity event" unlike anything that we have seen since the collapse of Lehman Brothers back in 2008.

At one point on Friday, Deutsche Bank stock fell below the 10 euro mark for the first time ever before bouncing back a bit. A completely unverified rumor that was spreading on Twitter that claimed that Deutsche Bank would settle with the Department of Justice for only 5.4 billion dollars was the reason for the bounce.

But the size of the fine is not really the issue now. Shares of Deutsche Bank have fallen by more than half so far in 2016, and this latest episode seems to have been the final straw for the deeply troubled financial institution. Old sources of liquidity are being cut off, and nobody wants to be the idiot that offers Deutsche Bank a new source of liquidity at this point.

As a result, Deutsche Bank is potentially facing a "liquidity event" on a scale that we have not seen since the financial crisis of 2008. The following comes from Zero Hedge...

It is not solvency, or the lack of capital - a vague, synthetic, and usually quite arbitrary concept, determined by regulators - that kills a bank; it is - as Dick Fuld will tell anyone who bothers to listen - the loss of (access to) liquidity: cold, hard, fungible (something Jon Corzine knew all too well when he commingled and was caught) cash, that pushes a bank into its grave, usually quite rapidly: recall that it took Lehman just a few days for its stock to plunge from the high double digits to zero.

It is also liquidity, or rather concerns about it, that sent Deutsche Bank stock crashing to new all time lows earlier today: after all, the investing world already knew for nearly two weeks that its capitalization is insufficient.

As we reported earlier this week, it was a report by Citigroup, among many other, that found how badly undercapitalized the German lender is, noting that DB's "leverage ratio, at 3.4%, looks even worse relative to the 4.5% company target by 20183 and calculated that while he only models ¬2.9bn in litigation charges over 2H16-2017 - far less than the $14 billion settlement figure proposed by the DOJ - and includes a successful disposal of a 70% stake in Postbank at end-2017 for 0.4x book he still only reaches a CET 1 ratio of 11.6% by end-2018, meaning the bank would have a Tier 1 capital ¬3bn shortfall to the company target of 12.5%, and a leverage ratio of 3.9%, resulting in an ¬8bn shortfall to the target of 4.5%.

The more the stock price drops, the faster other financial institutions, investors and regular banking clients are going to want to pull their money out of Deutsche Bank. And every time there is news about people pulling money out of the bank, that is just going to drive the stock price even lower.

In other words, Deutsche Bank may be entering a death spiral that may be impossible to stop without a government bailout, and the German government has already stated that there will be no bailout for Deutsche Bank.

Banking customers have a total of approximately 566 billion euros deposited with the bank, and even if a small fraction of those clients start demanding their money back it is going to cause a major, major crunch.

Deutsche Bank CEO John Cryan attempted to calm nerves on Friday by releasing a memo to employees that blamed "speculators" for the decline in the stock price...

Instead of doing what many have correctly suggested he should be doing, namely focusing on ways to raise more capital for the undercapitalized Deutsche Bank in order to stem the slow (at first) liquidity leak, first thing this morning CEO John Cryan issued another morale-boosting note to employees of Deustche Bank who have been watching their stock price crash to another record low, dipping under ¬10 in early trading for the first time ever.

In the memo the embattled CEO worryingly did what Dick Fuld and other chief executives did when they felt the situation slipping out of control, namely blaming evil "rumor-spreading" shorts, saying "our bank has become subject to speculation. Ongoing rumours are causing significant swings in our stock price. ... Trust is the foundation of banking. Some forces in the markets are currently trying to damage this trust."

Just as important, Cryan confirms the Bloomberg report that "a few of our hedge fund clients have reduced some activities with us. That is causing unjustified concerns."

As we explained last night, the concerns are very much justified if they spread to the biggest risk-factor for the German bank: its depositors, which collectively hold over ¬550 billion in liquidity-providing instruments.

One of the reasons why Deutsche Bank is considered to be so systemically "dangerous" is because it has 42 trillion euros worth of exposure to derivatives. That is an amount of money that is 14 times larger than the GDP of the entire nation of Germany.

Some firms that were derivatives clients of the bank have already gotten spooked and have moved their business to other institutions. It was this report from Bloomberg that really helped drive down the stock price of Deutsche Bank earlier this week...

The funds, a small subset of the more than 800 clients in the bank's hedge fund business, have shifted part of their listed derivatives holdings to other firms this week, according to an internal bank document seen by Bloomberg News.

Among them are Izzy Englander's $34 billion Millennium Partners, Chris Rokos's $4 billion Rokos Capital Management, and the $14 billion Capula Investment Management, said a person with knowledge of the situation who declined to be identified talking about confidential client matters.

"The issue here is now one of confidence," said Chris Wheeler, a financial analyst with Atlantic Equities LLP in London.

So what comes next?

Monday is a banking holiday for Germany, so we may not see anything major happen until Tuesday.

An announcement of a major reduction in the Department of Justice fine may buy Deutsche Bank some time, but any reprieve would likely only be temporary.

What appears to be more likely is the scenario that Jeffrey Gundlach is suggesting...

But Jeffrey Gundlach, chief executive of DoubleLine Capital, said investors betting that Berlin would not rescue Deutsche could find themselves nursing big losses.

'The market is going to push down Deutsche Bank until there is some recognition of support. They will get assistance, if need be,' said Gundlach, who oversees more than $100 billion at Los Angeles-based DoubleLine.

It will be very interesting to see how desperate things become before the German government finally gives in to the pressure.

The complete and total collapse of Deutsche Bank would be an event many times more significant for the global financial system than the collapse of Lehman Brothers was.

Global leaders simply cannot afford for such a thing to happen, but without serious intervention it appears that is precisely where we are heading.

Personally, I don't know exactly what will happen next, but it will be fascinating to watch

Read more at http://www.prophecynewswatch.com/articl ... ue6xUhV.99

-

Blue Frost

- SUPER VIP

- Posts: 98158

- Joined: May 14th, 2012, 1:01 am

- Location: Yodenheim

Re: The Coming Financial Meltdown

Looks bad for them, and the country thanks to the elitist robbing us all. How can they pay for all those invaders, the sorry bums they already had, and keep running also.

My guess the looting by the rich has took it's toll the most.

My guess the looting by the rich has took it's toll the most.

"Being alone isn't what hurts. It's when the people around you make you feel alone" ~ Naruto Uzumaki, an Anime Character

Re: The Coming Financial Meltdown

Canada I believe is doing better than most countries but we too are starting to feel the pinch

.The Noose Is Tightening Quickly On The Global Economy

By Brandon Smith/Daily Sheeple October 06, 2016

The investment world has an embarrassingly short attention span. But frankly, it is a necessity. If daytraders, hedge funds and other horses in the carousel actually had to look beyond the next week of market activity or study back on market history in comparison to today, then they would not be able to retain their blind optimism, which is exactly what is necessary for them to continue functioning.

If they were all to examine the global financial situation with any honesty, the entire facade would collapse tomorrow.

At bottom, it is not central bank stimulus and intervention alone that drives equities and bond markets; it is the naive faith and willful ignorance of average market participants. There is a problem with this kind of economic model, however. Reality is never kept in check indefinitely. Fiscal truths will be exposed, one way or another.

How does one know when this full spectrum shift in awareness will occur? Well, there's no science that can help us with that. While basic economics is subject to the forces of supply, demand and mathematical inevitability, it is also subject to human psychology, which is another matter entirely.

In the past I have made a point to outline similarities in responses to various economic crises. For example, the media response and public perception at the onset of the Great Depression was a highly unfortunate exercise in false optimism.

The response just before the credit crash of 2008 by the media and the masses was much the same. It is interesting to note in particular that the mainstream media tends to become more over-the-top in its certainty of economic stability the closer the system comes to collapse.

That is to say, the nearer we edge towards financial calamity, the more violently the mainstream media attacks people who suggest that danger is on the horizon.

Notice any striking similarities between the mainstream rhetoric of 2006/2007 and the mainstream rhetoric of today? Notice how emotionally aggressive and almost desperate the media becomes when maintaining market faith, rather than looking at the situation objectively as the fundamentals begin to overwhelm investor complacency?

To be clear, while mainstream economists are almost always wrong, independent analysts are not prophets. We usually cannot provide the exact timing for the economic shifts we see coming. All we can do is provide a general window in which the events are likely to take place.

Peter Schiff's predictions on how the housing bubble and the credit crisis would play out were absolutely correct, even though he was about six months to eight months off his timing. Again, this is not an exact science, and human psychology has the ability to offset market fundamentals for months.

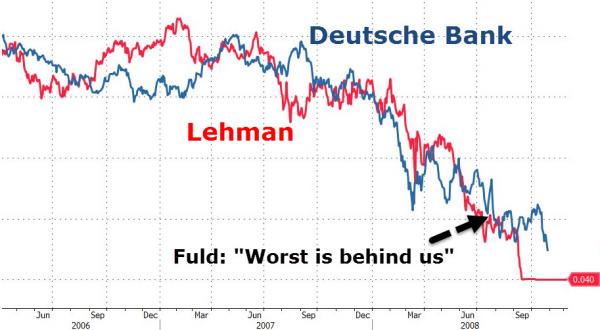

The supposed "catalyst" for the 2008 crash is primarily attributed to the fall of Lehman Brothers. I highly recommend any of the "bullish" economists out there arguing today that the central banks intend to prolong a stock rally indefinitely examine the statements made in the mainstream about Lehman and by Lehman leading up to their eventual death rattle. Then, absorb and really think on some of the recent statements and tactics used by Germany's Deutsche Bank.

Specifically, note Lehman's use of accounting and derivatives gimmicks and the cycling of funds through various accounts in order to make the company appear solvent. Then, take a look at revelations coming out of places like Italy that Deutsche Bank has been using the same model of false accounts and market manipulation, once again, with derivatives as a main tool for fraud.

Also notice the same outright dismissals of all pertinent evidence that Deutsche Bank might be suffering a capital shortfall, as Chief Executive John Cryan blames "speculators" for the companies losses.

Lehman's Dick Fuld and Bear Stearns' Jimmy Cain both blamed "speculators" and "rumors and conspiracies" for the fall of their companies during the derivatives debacle eight years ago. It would seem that history doesn't just rhyme, it sometimes repeats exactly.

Below is a rather revealing chart from the folks at Zero Hedge comparing the collapse of Lehman Brothers stock value to the steady decline of Deutsche Bank. Check it out:

image: https://plnami.blob.core.windows.net/me ... utsche.jpg

To be clear, Lehman was no catalyst. It was only a litmus test for a system completely devoid of tangible value and drowning in toxic debt. Lehman was a part of a much larger problem, it was not the cause of the problem. The same is true for Deutsche Bank.

The panic growing around Germany's second largest financial institution, Commerzbank, as it moves to lay off nearly 10,000 employees and suspend its dividend is another crisis indicator separate from Deutsche Bank. The clear solvency issues in Italy's major banks, including Monte dei Paschi, are yet another explosive element.

Keep in mind that when these edifices begin to crumble and Europe enters a state of financial emergency, the mainstream media and numerous governments will continue to blame speculators. They will also claim that the entire disaster was set in motion through a "domino effect"; the first domino probably being Deutsche Bank. This will be a lie. There is no line of dominoes.

One bank will not be bringing down the other banks -- yes, there is terrible interdependency, but the real issue is that ALL of these banks are falling due to their own cancerous behaviors. The very system they are built around is a corrupt and unsustainable model, and I hold that this is by design.

International financiers do not want the general public to look at the validity of the system, they want the public to view collapse events as an oversimplified case of cause and effect.

If the public were to understand that the global banking model is a destructive one (for the public, not for the elites), then they might demand the erasure of the model and its institutions entirely.

The elites don't want that. What they want is to be free to conjure crisis after crisis after crisis; to have the option to collapse the system only to replace it with something identical in nature but even more oppressive in its function. They want to create chaos today so that greater centralization can be purchased in the future through mass fear.

I continue to maintain as I always have that central banks around the world are shifting strategies and will do very little to intervene from this point on in the propping up of insolvent banking groups or equities markets. It is very unlikely that Germany or the European Central Bank, for example, will move to infuse Deutsch Bank with capital (at least, not until the damage has already been done).

It is also unlikely that any central bank will move to openly stimulate markets until an equities crash has run its course. In fact, some central banks including the Federal Reserve may act to expedite a stock crash -- watch for this to occur if Donald Trump attains the White House.

This has all happened before. It happened in 2008 when the Federal Reserve stepped back and allowed Lehman Brothers to go bankrupt. It will probably happen again when the German government and the ECB refuse to back Deutsche Bank.

The noose is tightening on the global economy and, once again, the mainstream media is too biased or too dumb to see it. They'll accuse the alternative media of crying "doom and gloom," and perhaps our timing will be off.

But exact timing will not really matter once the house of cards begins to topple. If we stick to our positions and refuse to be intimidated by rhetoric, the time will come when people will only remember that we were right for the most part and that the mainstream media was incompetent or dishonest.

In the meantime, we have a whole swarm of other trigger events before the end of the year. I predicted in my article The World Is Turning Ugly As 2016 Winds Down that the Saudi 9/11 bill might be vetoed by Obama and that the veto would be overturned by the Senate.

This has now taken place, which means increased Saudi tensions with the U.S. resulting in the eventual demise of the dollar's petro-currency status.

Watch the coming Italian constitutional referendum which could pave the way for conservative movements to initiate an Italian version of the Brexit. Also keep an eye on Syria yet again as diplomatic conflict flares between the U.S. and Russia (gee, who didn't see that coming?).

And, of course, the U.S. presidential election which appears to be culminating into the most divisive political event in America in decades.

Ignore the delusional positivism of the mainstream media and a large part of the equities trading community. Their fantasies only grow more elaborate the closer we get to a market heart attack. And remember, economic collapse is a process, not an overnight affair.

The progression of global decline should be apparent to anyone paying attention since 2008. The only question is, when will the average citizen become aware? My feeling according to current trends is, very soon.

Originally published at the Daily Sheeple - reposted with permission.

Read more at http://www.prophecynewswatch.com/articl ... WCGfRH3.99

.The Noose Is Tightening Quickly On The Global Economy

By Brandon Smith/Daily Sheeple October 06, 2016

The investment world has an embarrassingly short attention span. But frankly, it is a necessity. If daytraders, hedge funds and other horses in the carousel actually had to look beyond the next week of market activity or study back on market history in comparison to today, then they would not be able to retain their blind optimism, which is exactly what is necessary for them to continue functioning.

If they were all to examine the global financial situation with any honesty, the entire facade would collapse tomorrow.

At bottom, it is not central bank stimulus and intervention alone that drives equities and bond markets; it is the naive faith and willful ignorance of average market participants. There is a problem with this kind of economic model, however. Reality is never kept in check indefinitely. Fiscal truths will be exposed, one way or another.

How does one know when this full spectrum shift in awareness will occur? Well, there's no science that can help us with that. While basic economics is subject to the forces of supply, demand and mathematical inevitability, it is also subject to human psychology, which is another matter entirely.

In the past I have made a point to outline similarities in responses to various economic crises. For example, the media response and public perception at the onset of the Great Depression was a highly unfortunate exercise in false optimism.

The response just before the credit crash of 2008 by the media and the masses was much the same. It is interesting to note in particular that the mainstream media tends to become more over-the-top in its certainty of economic stability the closer the system comes to collapse.

That is to say, the nearer we edge towards financial calamity, the more violently the mainstream media attacks people who suggest that danger is on the horizon.

Notice any striking similarities between the mainstream rhetoric of 2006/2007 and the mainstream rhetoric of today? Notice how emotionally aggressive and almost desperate the media becomes when maintaining market faith, rather than looking at the situation objectively as the fundamentals begin to overwhelm investor complacency?

To be clear, while mainstream economists are almost always wrong, independent analysts are not prophets. We usually cannot provide the exact timing for the economic shifts we see coming. All we can do is provide a general window in which the events are likely to take place.

Peter Schiff's predictions on how the housing bubble and the credit crisis would play out were absolutely correct, even though he was about six months to eight months off his timing. Again, this is not an exact science, and human psychology has the ability to offset market fundamentals for months.

The supposed "catalyst" for the 2008 crash is primarily attributed to the fall of Lehman Brothers. I highly recommend any of the "bullish" economists out there arguing today that the central banks intend to prolong a stock rally indefinitely examine the statements made in the mainstream about Lehman and by Lehman leading up to their eventual death rattle. Then, absorb and really think on some of the recent statements and tactics used by Germany's Deutsche Bank.

Specifically, note Lehman's use of accounting and derivatives gimmicks and the cycling of funds through various accounts in order to make the company appear solvent. Then, take a look at revelations coming out of places like Italy that Deutsche Bank has been using the same model of false accounts and market manipulation, once again, with derivatives as a main tool for fraud.

Also notice the same outright dismissals of all pertinent evidence that Deutsche Bank might be suffering a capital shortfall, as Chief Executive John Cryan blames "speculators" for the companies losses.

Lehman's Dick Fuld and Bear Stearns' Jimmy Cain both blamed "speculators" and "rumors and conspiracies" for the fall of their companies during the derivatives debacle eight years ago. It would seem that history doesn't just rhyme, it sometimes repeats exactly.

Below is a rather revealing chart from the folks at Zero Hedge comparing the collapse of Lehman Brothers stock value to the steady decline of Deutsche Bank. Check it out:

image: https://plnami.blob.core.windows.net/me ... utsche.jpg

{kind=link}

To be clear, Lehman was no catalyst. It was only a litmus test for a system completely devoid of tangible value and drowning in toxic debt. Lehman was a part of a much larger problem, it was not the cause of the problem. The same is true for Deutsche Bank.

The panic growing around Germany's second largest financial institution, Commerzbank, as it moves to lay off nearly 10,000 employees and suspend its dividend is another crisis indicator separate from Deutsche Bank. The clear solvency issues in Italy's major banks, including Monte dei Paschi, are yet another explosive element.

Keep in mind that when these edifices begin to crumble and Europe enters a state of financial emergency, the mainstream media and numerous governments will continue to blame speculators. They will also claim that the entire disaster was set in motion through a "domino effect"; the first domino probably being Deutsche Bank. This will be a lie. There is no line of dominoes.

One bank will not be bringing down the other banks -- yes, there is terrible interdependency, but the real issue is that ALL of these banks are falling due to their own cancerous behaviors. The very system they are built around is a corrupt and unsustainable model, and I hold that this is by design.

International financiers do not want the general public to look at the validity of the system, they want the public to view collapse events as an oversimplified case of cause and effect.

If the public were to understand that the global banking model is a destructive one (for the public, not for the elites), then they might demand the erasure of the model and its institutions entirely.

The elites don't want that. What they want is to be free to conjure crisis after crisis after crisis; to have the option to collapse the system only to replace it with something identical in nature but even more oppressive in its function. They want to create chaos today so that greater centralization can be purchased in the future through mass fear.

I continue to maintain as I always have that central banks around the world are shifting strategies and will do very little to intervene from this point on in the propping up of insolvent banking groups or equities markets. It is very unlikely that Germany or the European Central Bank, for example, will move to infuse Deutsch Bank with capital (at least, not until the damage has already been done).

It is also unlikely that any central bank will move to openly stimulate markets until an equities crash has run its course. In fact, some central banks including the Federal Reserve may act to expedite a stock crash -- watch for this to occur if Donald Trump attains the White House.

This has all happened before. It happened in 2008 when the Federal Reserve stepped back and allowed Lehman Brothers to go bankrupt. It will probably happen again when the German government and the ECB refuse to back Deutsche Bank.

The noose is tightening on the global economy and, once again, the mainstream media is too biased or too dumb to see it. They'll accuse the alternative media of crying "doom and gloom," and perhaps our timing will be off.

But exact timing will not really matter once the house of cards begins to topple. If we stick to our positions and refuse to be intimidated by rhetoric, the time will come when people will only remember that we were right for the most part and that the mainstream media was incompetent or dishonest.

In the meantime, we have a whole swarm of other trigger events before the end of the year. I predicted in my article The World Is Turning Ugly As 2016 Winds Down that the Saudi 9/11 bill might be vetoed by Obama and that the veto would be overturned by the Senate.

This has now taken place, which means increased Saudi tensions with the U.S. resulting in the eventual demise of the dollar's petro-currency status.

Watch the coming Italian constitutional referendum which could pave the way for conservative movements to initiate an Italian version of the Brexit. Also keep an eye on Syria yet again as diplomatic conflict flares between the U.S. and Russia (gee, who didn't see that coming?).

And, of course, the U.S. presidential election which appears to be culminating into the most divisive political event in America in decades.

Ignore the delusional positivism of the mainstream media and a large part of the equities trading community. Their fantasies only grow more elaborate the closer we get to a market heart attack. And remember, economic collapse is a process, not an overnight affair.

The progression of global decline should be apparent to anyone paying attention since 2008. The only question is, when will the average citizen become aware? My feeling according to current trends is, very soon.

Originally published at the Daily Sheeple - reposted with permission.

Read more at http://www.prophecynewswatch.com/articl ... WCGfRH3.99

Re: The Coming Financial Meltdown

I believe that we are doing a bit better in Canada. But with Justin Trudeau in office now this will probably change for the worse soon.

Two-Thirds Will Be Out Of Cash Almost Immediately If Economic Crisis Hits

Did you know that almost 70 percent of the U.S. population is essentially living paycheck to paycheck?

As you will see below, a brand new survey has found that 69 percent of all Americans have less than $1,000 in savings. Of course one of the primary reasons for this is that most of us are absolutely drowning in debt.

In fact, the total amount of household debt in the United States now exceeds 12 trillion dollars. So many Americans are so busy just trying to pay off their existing debts that they can't even think about saving anything for the future.

If economic conditions remain relatively stable, the fact that so many of us are living on the edge probably won't kill us. But the moment the economy plunges into another 2008-style crisis (or worse), we could be facing a situation where two-thirds of the country is in imminent danger of running out of cash.

If you are living paycheck to paycheck, you live under the constant threat of your life being totally turned upside down if that paycheck ever goes away. During the last crisis, millions of Americans lost their jobs very rapidly, and because so many of them were living paycheck to paycheck all of a sudden large numbers of people couldn't pay their mortgages.

As a result, multitudes of American families went through the extremely painful process of foreclosure.

Unfortunately, it appears that we have not learned anything from the last go around. According to the brand new survey that I mentioned above, 69 percent of all Americans have less than $1,000 in savings...

Last year, GoBankingRates surveyed more than 5,000 Americans only to uncover that 62% of them had less than $1,000 in savings. Last month GoBankingRates again posed the question to Americans of how much they had in their savings account, only this time it asked 7,052 people.

The result? Nearly seven in 10 Americans (69%) had less than $1,000 in their savings account.

Breaking the survey data down a bit further, we find that 34% of Americans don't have a dime in their savings account, while another 35% have less than $1,000. Of the remaining survey-takers, 11% have between $1,000 and $4,999, 4% have between $5,000 and $9,999, and 15% have more than $10,000.

Perhaps the most alarming fact from this survey is that 62 percent of all Americans had less than $1,000 in savings last year. So that means that this number has gotten 7 percent worse over the last 12 months.

How did that happen? I thought the mainstream media was telling us that the economy was getting better...

Look, if you don't have an emergency fund you are in danger of losing everything. This is a point that I have been making over and over again for years, and in an article about this new survey USA Today made this point very strongly as well...

This data is particularly worrisome since the recommendation is for Americans to have six months in expenses saved in case of an emergency, such as a large medical expense, car repair bill, or losing your job. Without this emergency fund to fall back on, millions of Americans could be risking financial disaster.

As the publisher of The Economic Collapse Blog, people are constantly asking me what they should do to get prepared for what is coming.

The number one thing that I always suggest is to build up an emergency fund.

In a chaotic situation it is always hard to anticipate accurately what is going to happen, but without a doubt we are all going to need to continue to pay our bills and to buy things for our families during the next crisis.

Yes, someday the U.S. dollar will become rather worthless, but until that happens you are going to need to continue to put a roof over the heads of your family and to put food on the table.

And you are going to need money to do those things.

Some time ago, the Federal Reserve also found that a large percentage of Americans are living on the edge of financial disaster.

They discovered that 47 percent of all Americans could not even come up with $400 to pay for an unexpected emergency room visit without borrowing the money or selling something that they own.

If you can't even come up with $400 you are really hurting, but that is the status of about half the country these days.

We are continually being told that the economy is strong, but that is simply not the truth.

In fact, it turns out that the period from 2005 to 2015 was the worst period for per capita real GDP growth in modern American history. The following comes from Zero Hedge...

Growth was unusually strong in the 1960s and early 1970s. In every year from 1966 through 1973, per-capita income was up between 30 percent and 40 percent from a decade earlier. Thus, it's not surprising that many Americans recall this as a great period for the nation's economy.

In every year from 1984 to 2007 -- a period that economists call the Great Moderation, because of the way both growth and interest rates stabilized -- per-person income was up between 20 percent and 30 percent from a decade earlier. That's ample reason for Americans to view this as a good period for the economy.

Cumulative per-person growth from 2005 to 2015 was lower than in any prior decade in the sample. That certainly helps explain why many Americans are unhappy with the nation's recent economic performance

And as I repeat over and over, Barack Obama is on track to be the one and only president in all of American history to never have a single year when the economy grew by at least 3 percent, and he has had eight years to try to accomplish that feat.

Why doesn't Donald Trump ever bring up that amazing fact? I would think that he could get a lot of mileage out of that number.